The Fringe Benefits Tax (FBT) year ending 31 March 2025 introduces important compliance challenges for Australian employers and tax advisors. For members of CA ANZ, CPA Australia, and the Institute of Public Accountants (IPA), understanding the latest FBT rules is essential to offering accurate, compliant advice and meeting CPD requirements.

This article outlines key changes, compliance priorities, and educational resources to help accounting professionals manage their FBT obligations effectively in 2025.

Key FBT Changes for 2025

According to the Australian Taxation Office (ATO), the FBT rate remains at 47%, but important developments around vehicles, documentation, and ATO interpretations demand closer attention.

Electric and Plug-in Hybrid Vehicles

According to ATO, from 1 April 2025, plug-in hybrid electric vehicles (PHEVs) will no longer be FBT-exempt, unless part of a financially binding arrangement entered into before this date and unchanged thereafter.

Electric vehicles (EVs) powered by battery or hydrogen fuel cell technology remain exempt, subject to:

-

First held and used on or after 1 July 2022

-

Value below the Luxury Car Tax threshold ($89,332 for the 2023–24 income year)

Even when exempt, EVs must have their notional taxable value included in the employee’s Reportable Fringe Benefits Amount (RFBA).

The ATO’s Practical Compliance Guideline (PCG) 2024/2 allows a simplified method of calculating home charging costs—4.2 cents per kilometre. However, charging equipment itself is not covered by the exemption and may be a separate fringe benefit.

For a focused training on how EV exemptions, logbooks, and valuation rules interact, the course FBT: Valuations, Logbooks, and Electric Vehicle Exemptions offers a detailed and practical overview.

Alternative Record-Keeping from 1 April 2024

Effective from 1 April 2024, the ATO allows employers to use alternative forms of evidence, such as electronic records or third-party software outputs, instead of traditional employee declarations or travel diaries. However, the standard of substantiation remains high. For detailed updates on legislative changes and administrative developments, refer to the ATO’s “What’s new in FBT” page.

Practitioners can stay current on these evolving requirements through the FBT Updates 2024–2025 CPD package, which includes key legislative updates and ATO interpretations.

Car Parking Fringe Benefits

Car parking remains a priority area for ATO audits. Guidance is detailed in Taxation Ruling TR 2021/2, which covers how to determine whether a parking facility is commercial and how to correctly value the benefit.

The recent court decision in the Toowoomba Regional Council, which ruled against the ATO's interpretation of a commercial parking station in that specific case, is noteworthy, although the ATO has filed an appeal. This highlights the evolving nature of this area.

Non-Car Vehicles and Logbooks

According to PRICEWATERHOUSECOOPERS (PWC), the ATO is also increasing scrutiny on vehicles not classified as cars, such as dual-cab utes or minibuses. These may be exempt only when private use is truly minor, infrequent, and irregular. Supporting this claim requires accurate, contemporaneous logbooks, which continue to be a common source of compliance failures. Logbooks must be updated every five years or sooner if usage patterns change significantly. Incorrectly classifying a vehicle or understating private use can lead to significant FBT liabilities.

For professionals needing a technical refresher, the Fringe Benefit Tax (FBT) Review course delivers a comprehensive update on rules, categories, and practical compliance strategies.

Meal Entertainment and Expense Classification

Correctly distinguishing entertainment expenses from legitimate business costs remains difficult. Selecting the correct valuation method—such as the actual or 50/50 method—and understanding which is valid under salary packaging arrangements is critical. Documentation must clearly demonstrate the purpose and beneficiaries of such expenditures. The ATO provides detailed guidance on meal entertainment valuation methods.

Worker Classification and Lodgment

Fringe benefits generally apply only to employees. The ATO's Taxation Ruling (TR) 2023/4 outlines the approach for distinguishing employees from contractors, stressing the importance of assessing the full working relationship beyond written agreements.

Employers should also lodge an FBT return even when no tax is due—this starts the four-year amendment period and protects against prolonged audit exposure.

Valuation, Exemptions, and Reporting

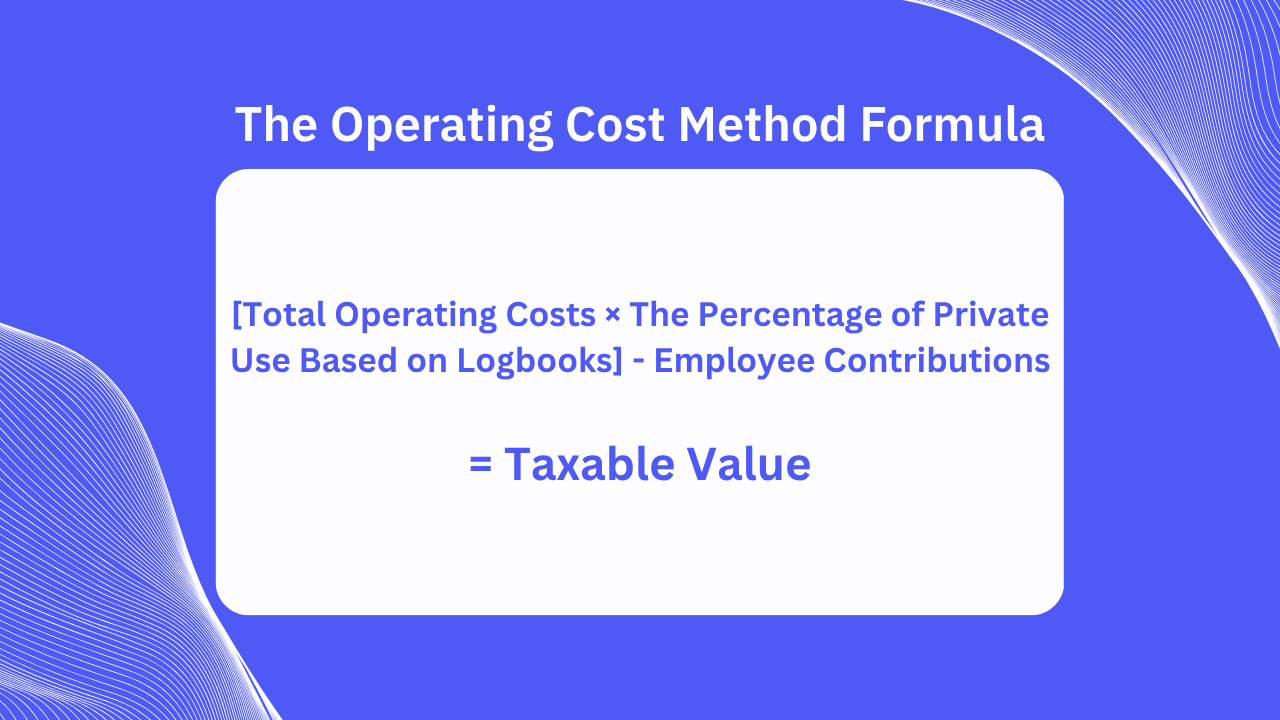

Fringe benefits fall under categories such as car, loan, housing, property, and entertainment. Each has specific valuation rules. For example, car benefits may be assessed using the statutory formula or the operating cost method based on private use percentage (via a logbook). Employee contributions, made from after-tax income, can reduce the taxable value if documented correctly.

If the total taxable value of benefits provided to an employee exceeds $2,000 in a year, the grossed-up value must be reported through Single Touch Payroll (STP). This includes benefits such as exempt EV use, and may impact government entitlements, child support, and Medicare levy obligations.

Ethical Standards and Professional Development

As required by the APES 110 Code of Ethics, accountants must act with integrity, objectivity, due care, confidentiality, and professionalism. FBT advice, especially in areas such as vehicle structuring or expense classification, must be legally sound and not geared toward aggressive avoidance.

Continuous professional development is essential to uphold these standards. CPD-compliant FBT resources, such as LearnFormula, are valuable for staying ahead of changing tax rules and interpretations.

Conclusion

The FBT landscape for 2025 presents both ongoing complexities and specific new challenges, particularly concerning vehicle benefits and record-keeping. For Australian Chartered Accountants, CPAs, and IPA members, maintaining a high level of technical proficiency, adhering to strict ethical standards, and continuously developing professional skills are critical for navigating this environment successfully.

For a deeper understanding of FBT valuations, exemptions, logbooks, and compliance strategies, explore our curated CPD courses on LearnFormula. Stay current, fulfill your professional development requirements, and strengthen your advisory capabilities with expert-led, up-to-date FBT training.